There are a number of key studies on the subject of receiving advice versus not receiving advice.

A study by Vanguard found that advisers can add over 3% per year in net returns for their clients. They cited behavioural coaching, spending strategy and rebalancing as the largest contributors. Their study also made the valid point that the most significant opportunities for an adviser to add value do not present themselves every year, hence the importance of an ongoing advice relationship.

Russel Investments estimated this to be as much as a 4.4% net increase in annual returns, through a combination of preventing behavioural mistakes, financial planning, tax smart advice and rebalancing

The International Longevity Center has been running a multi-year study on this topic. Here are their most pertinent conclusions:

“Taking advice has added £2.5bln to people’s savings and investments. An ongoing relationship with a financial adviser leads to better financial outcomes, those clients who received ongoing advice had pension wealth 50% greater than those who took one-off advice or none at all. The benefits of advice outweigh any costs associated with it. Once clients understand this it will no longer be seen as expensive. The simple fact is those who take advice are likely to be richer in retirement”

The University of Montreal estimated that the savings of an advised client will be over 2.73X larger over a 15-year period versus a non-advised client. Even over a shorter time frame of 5 years, an advised client will achieve a savings pot 1.58x the size of a non-advised client.

These are significant differences indeed. It is worth noting of course that not all advice is equal and there are many less than perfect advisers out there. It is certainly important to do your due diligence on the advisory company.

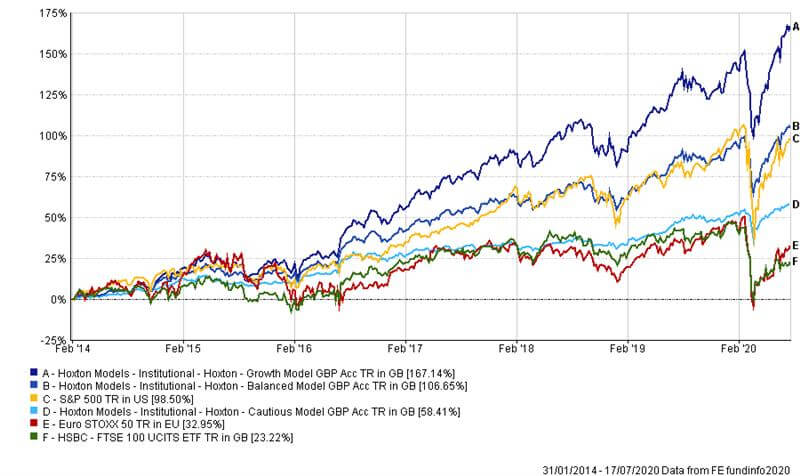

Below is a chart showing the performance of our model portfolios. These use a combination of both actively managed funds and ETFs, so the cost is kept down but they can still benefit from the managers that do outperform.