If the plan is to reduce quantitative easing, then it would mean slowing economic growth and negatively impacting market sentiment. We would expect a rotation back to defensive stocks such as technology and consumer staples if this becomes a reality. Naturally, a well-diversified portfolio covers all eventualities and that is the position we take because having a neutral approach during uncertain times is more defensive and especially with pensions it is the correct approach to have as a lot of these sectors are cyclical.

Jobs in the US are still a concern even though there have been a substantial number of jobs being created over the last few months. For example, there were over 850,000 jobs created in June and a massive 9 million openings in May. Even though this occurred, it is estimated that job increases would take at least another year to restore employment to pre-pandemic levels.

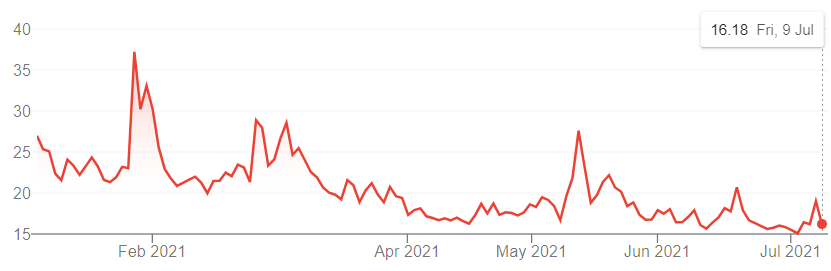

If the impact of the US market is considered substantial there may initiate a switch to safer assets including government backed assets. There is no real way to tell exactly what is going to happen and we have seen the negative impacts of moving to safer assets which naturally leads to the opportunity cost of missing out on growth it the market moves in a positive way. The best course of action to take is to stay true to our risk profiles and spend time in the markets rather than trying to time them.

International Markets

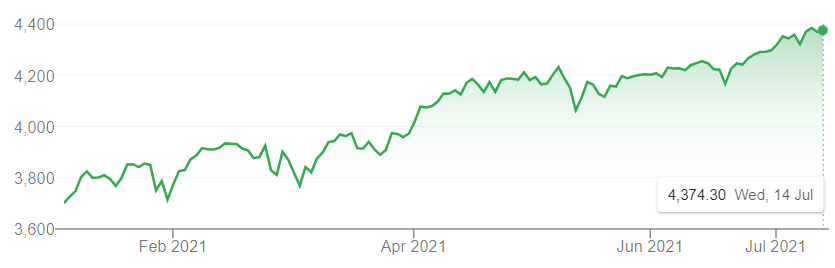

International markets also have been impacted positively by recent growth due to declines in covid cases, rising vaccination rates, and travel resuming. Major markets performed well over the later stage at the end of June off the back of hopes of a global recovery, although they generally lagged the US market.

I look forward to speaking with you before the end of the year at your next portfolio review. We have had a lot of questions about wider financial planning needs, and it would be great to speak with you about the best way to save for meaningful events. This could be anything from saving for children’s university fees or legacy planning to ensure your capital is set up correctly to be passed on to your loved ones if anything unexpected happens. If there are any planning events happening that you would like to discuss, then please contact us to set up a review call.