So our purchasing power is eroded year-on-year, meaning we have to spend more or consume less to maintain a balance.

To “encourage” us to spend more, governments and central banks set low nominal interest rates. This condition in which inflation is higher than the nominal interest rate produces negative real rates (known as the Fisher Effect).

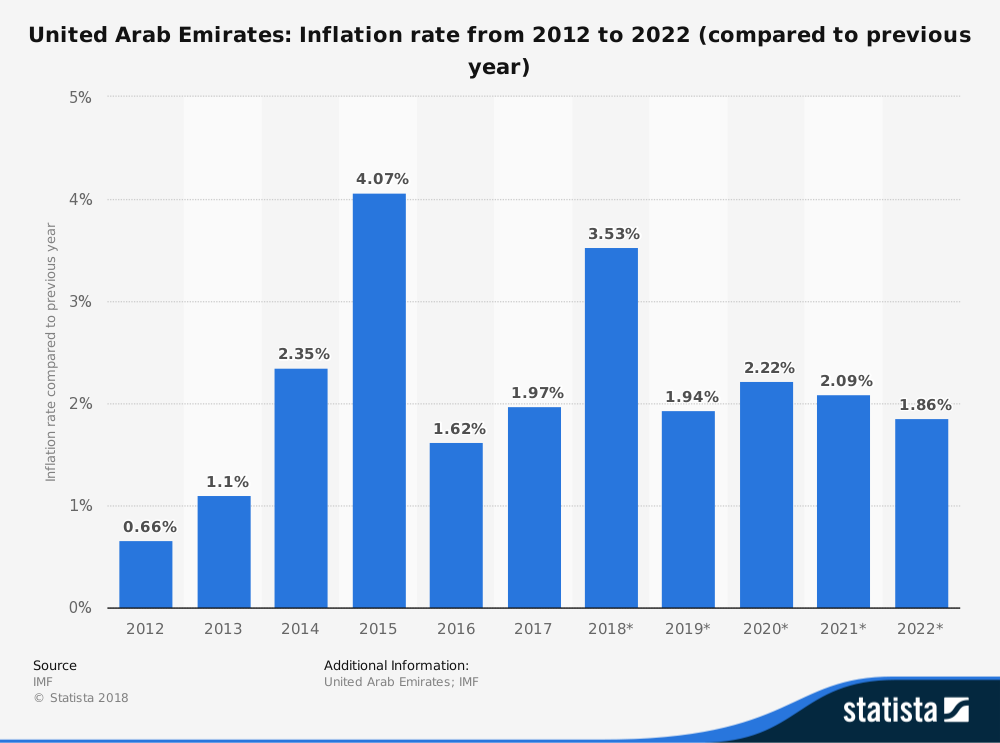

A well-known, high street bank here in the UAE offers a nominal interest rate of 0.25% p.a. on its standard savings account, calculated on the monthly balance. Therefore, the real interest rate will be negative at 1.69%.

In a simple interest scenario, a savings amount of $1,000 would earn $30.00 in nominal interest.

1000 × 0.0025 × 12

But the real purchasing power of that amount would be $797.20.

1000 × -0.0169 × 12

The same bank offers a fixed deposit account, with a top nominal interest rate of 2.05% over 60 months. Even this product will barely keep you up with inflation while tying up your capital.

So if keeping your money in a conventional bank savings account will cause a loss of the value of your savings in real terms, you cannot afford the cost of not investing.

How to outsmart the Fed?

The Fed would want us to invest in risky assets, such as stocks and real estate, to prop up collateral values in those markets. Indeed, the DJIA has increased almost 1,250% since 1986, while the S&P500 index has increased over 1,000%.

However, the stock market is volatile, and many savers are inherently conservative (with good reason). A 70-year old retiree doesn’t want to invest in stocks because he could easily lose 30% of his retirement savings when the next bubble bursts. A 22-year old professional saving for a down payment on his first property will avoid stocks for the same reason.

However, us savers have a range of alternatives that offer inflation-beating rates of return depending on the savings amount, comfortable risk profile and tenure. Our team is very knowledgeable about the current products on the market. Please get in touch and we can assist in finding the right products to meet your financial goals.