There are a few important details for cautious investors and the type of portfolio that is typically suitable for a cautious investment strategy. The main aim of the cautious strategy is capital preservation.

Capital Preservation

Preservation of capital is a conservative investment strategy where the primary goal is to prevent loss in a portfolio. Two major drawbacks of the capital preservation strategy are; the effect of inflation, and comparatively lower returns to equities from relatively safer investments over the long term.

The Role of Risk Tolerance

This ability to stomach volatile investments is commonly known as risk tolerance and is usually low for cautious investors. A cautious investor may be panicked by seeing their portfolio drop 20% in value and they may be willing to forego the potential for large gains in return for the security of their capital. If the portfolio dropped 2%, a cautious investor may be more able to stomach the small loss.

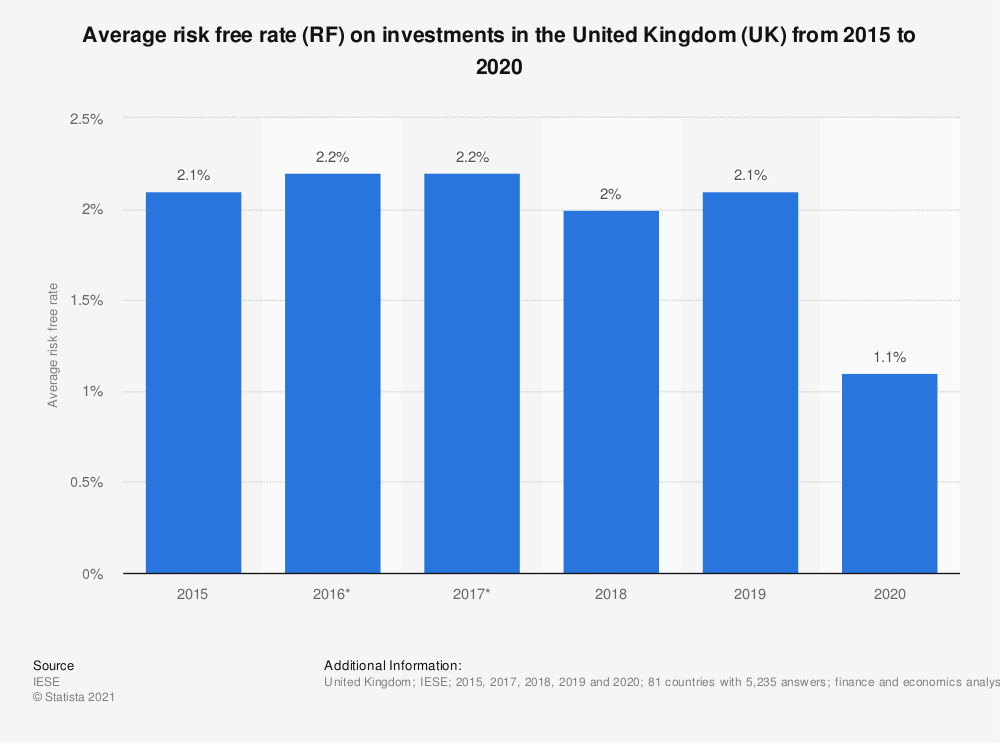

The Risk-Free Rate of Return

Firstly, it is important to understand what the risk-free rate means.

The risk-free rate of return refers to the theoretical rate of return of an investment with zero risk of financial loss. In practice, the risk-free rate of return does not truly exist, as every investment carries at least a small amount of risk. The current risk-free rate is approximately 1.1% in 2020 on average as shown by the below chart.

The average risk-free rate of return in the UK (2015-2020)