Secure and encrypted. Grow your wealth.

![]()

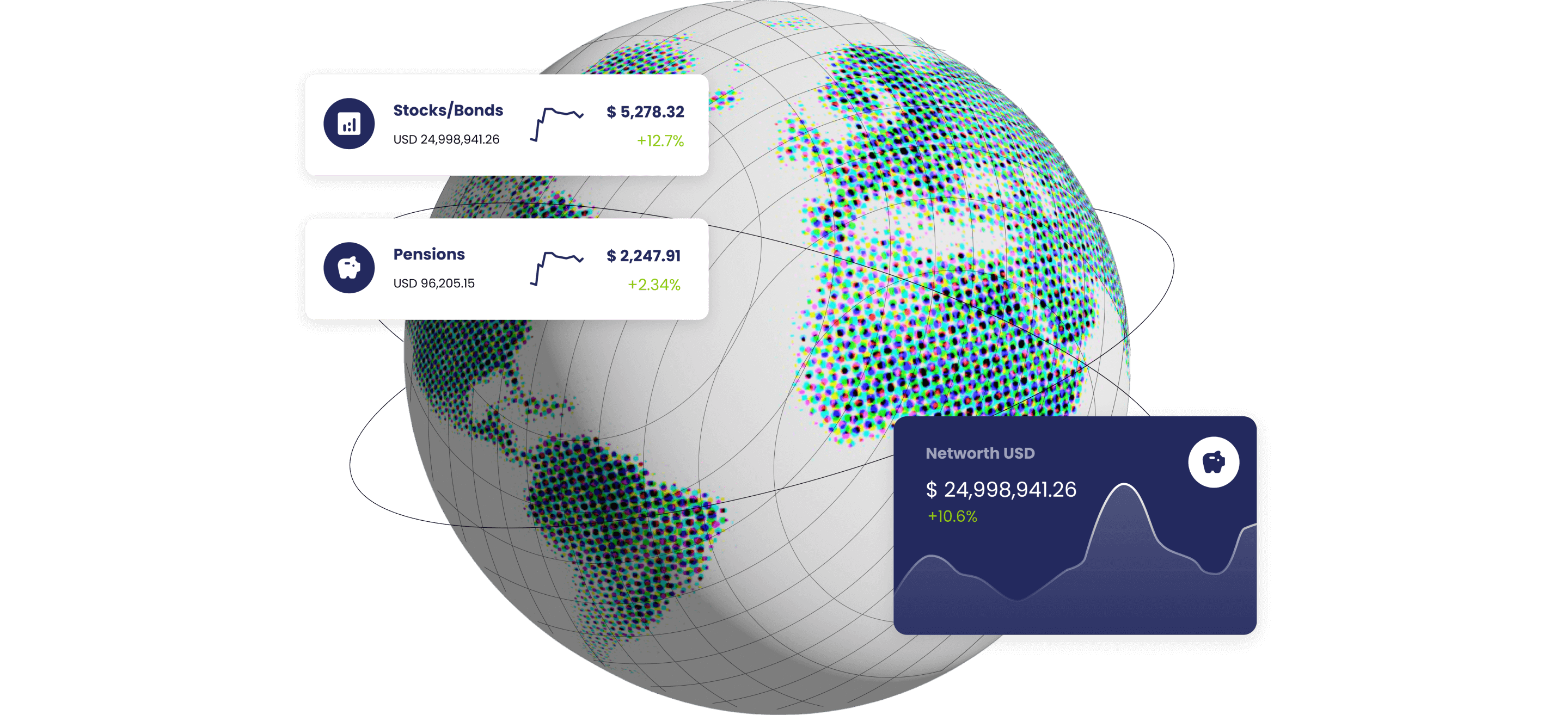

Track your Networth

Gain a clear understanding of your overall financial health. Our net worth tracking feature provides a consolidated view of your assets and liabilities, helping you make informed decisions to grow your wealth.

![]()

Retirement Calculator

Plan for a worry-free retirement with our powerful calculator. Estimate your future financial needs, set achievable retirement goals, and take proactive steps towards securing your financial future.

![]()

Track Bank Accounts

Effortlessly manage your bank accounts in one place. Keep an eye on your account balances, transaction history, and financial activity with ease and convenience.

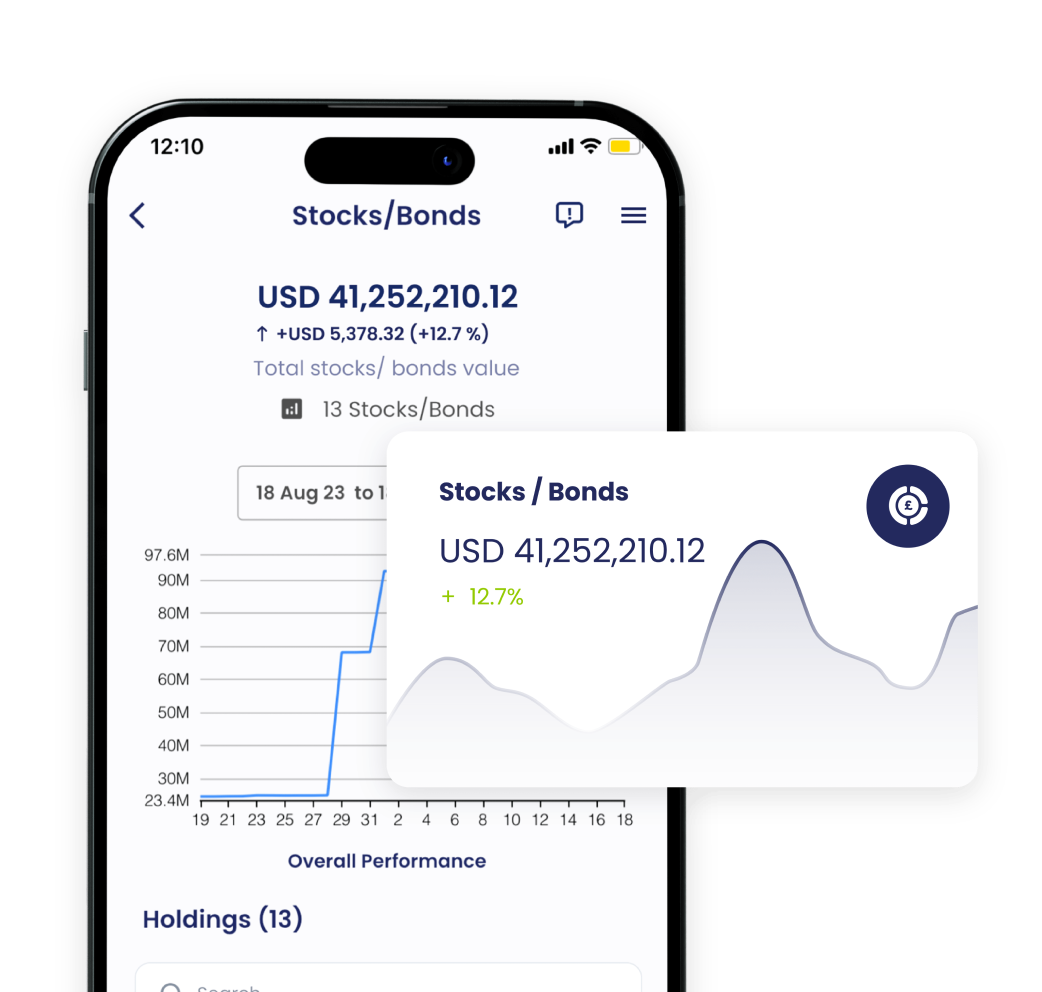

Track Stock Holdings

Stay informed about your stock investments. Monitor real-time market performance, track your stock portfolio, and make timely decisions to optimize your investments.

![]()

Track Crypto Holdings

Navigate the world of cryptocurrencies with confidence. Monitor your crypto holdings, track market prices, and ensure your digital assets are secure and growing.

![]()

Your Vault

Safeguard your important documents and information in a secure digital vault. Keep sensitive data, financial records, and vital documents protected and easily accessible whenever you need them.

Visit Website

Visit Website Write To Us

Write To Us

*This UK information is just contact details of the UK company, and this website is not the UK company’s website. If you are looking for more information on Hoxton Capital Management UK Ltd – you need to go to the UK website for UK residents by clicking here.

The information on this website is directed only at persons outside the United Kingdom and must not be acted upon by persons in the United Kingdom

*H Capital Financial Products and Promotion LLC is an affiliated entity and does not form part of the Hoxton Capital Management Group.

A strategic relationship between H Capital Financial Products Promotion LLC and certain Hoxton Capital Management Group entities exists so that investment promotion to any clients referred into the Hoxton Capital Management Group can take place for UAE residents.

*This UK information is just contact details of the UK company, and this website is not the UK company’s website. If you are looking for more information on Hoxton Capital Management UK Ltd – you need to go to the UK website for UK residents by clicking here.

The information on this website is directed only at persons outside the United Kingdom and must not be acted upon by persons in the United Kingdom

*H Capital Financial Products and Promotion LLC is an affiliated entity and does not form part of the Hoxton Capital Management Group.

A strategic relationship between H Capital Financial Products Promotion LLC and certain Hoxton Capital Management Group entities exists so that investment promotion to any clients referred into the Hoxton Capital Management Group can take place for UAE residents.