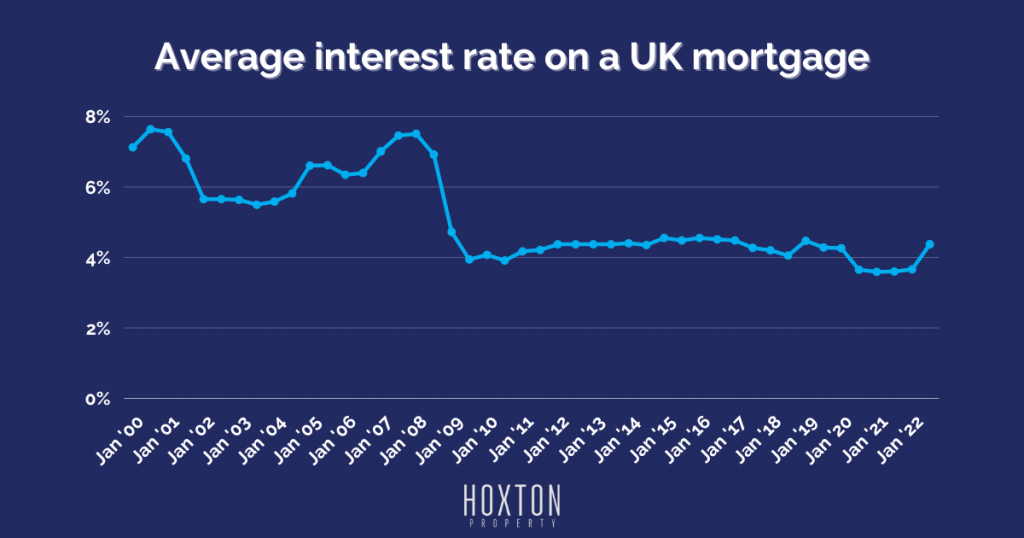

Currently, the average interest rate on a UK mortgage is 4.38%.

That’s still almost half the rate that borrowers were paying on average back in 2008. And it’s on a par with average rates over most of the 2010s.

Cautious investors may decide to wait to see what happens, hoping for a better rate to appear. This won’t happen.

Remember, whilst your capital is sitting in the bank, you’re losing money on it thanks to inflation.

As always, to get the best rates, property investors should still find the right deposit and have good credit ratings. This hasn’t changed. In the face of rising mortgage costs, it’s better to move now and secure your best rate than to delay.

How property protects investors from inflation

Property is often described as “inflation-proof”. But what does this mean?

It’s generally the rule that as inflation increases, so do property prices. As a tangible asset, the house or apartment an investor buys will always have value associated with it. Unlike a share, it would take truly exceptional circumstances for it to become worthless.

In a detailed analysis of the relationship between house prices and inflation, the Man Institute concluded that whilst there are different types of inflation (controlled inflation vs hyperinflation) that can affect house prices accordingly, they “expect any inflation in the coming years to be manageable and, if anything, supportive of house prices in many areas.”

In this way, inflation actually helps your capital grow when you invest in property.

On the other hand, if you’ve left your capital uninvested, inflation is slowly eating away at it.

Should you invest in UK property?

Our advice is not to wait to invest in UK property. Sitting on the fence during a time of high inflation isn’t going to help you financially.

We can help you by working on a cash flow projection that can answer any questions you might have about the likely performance of your investment over the next 10 years. If you’d like to have a no-obligation consultation with us, please get in touch.

The UK property market is still in a period of high growth and, although it may slow down, it has shown proven long-term resilience.