What is happening with global markets right now – Moheen Ahmed

Read here what Partner, Moheen Ahmed, had to say about the current global markets and his thoughts on inflation rates right now.

“As I am sure you are aware, global markets and economic conditions have continued to remain tough and volatile throughout 2022.

I understand that these tough times make difficult reading, however, I thought it would be best to continue to provide market updates and commentary to help provide context to the year so far.

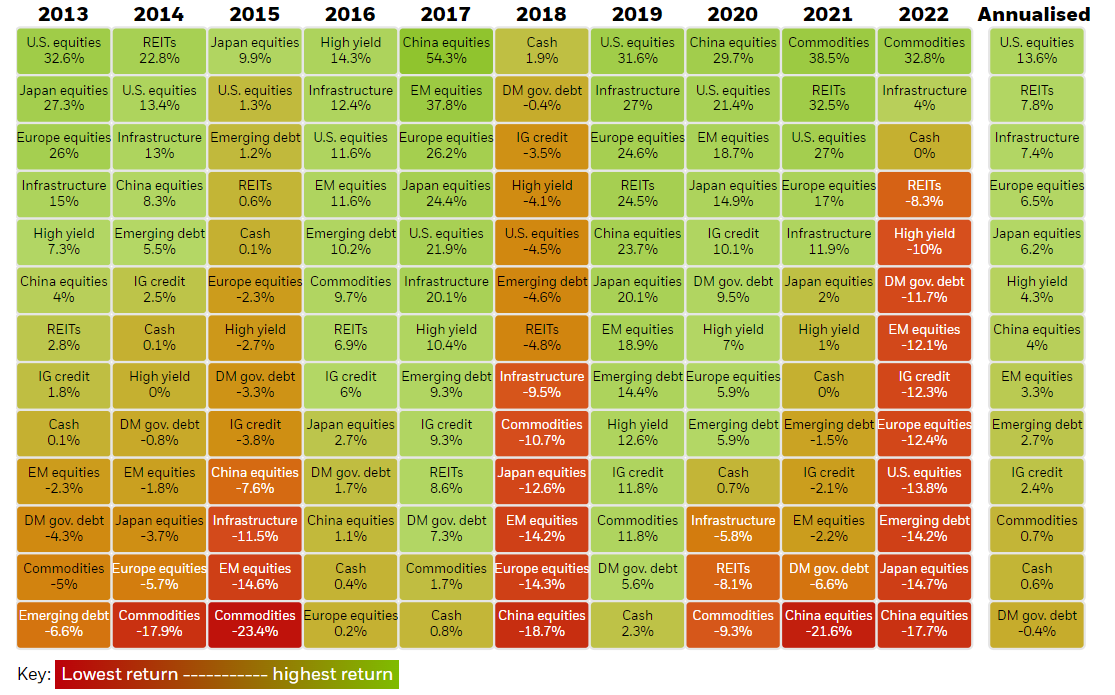

Below are the absolute returns for selected markets for every year from 2013 to 2022. These year to date figures are listed from best performing to worst performing sectors for each year according to Blackrock. As you can see, the year-to-date chart for 2022 makes grim reading. This year has been one of the worst starts to a year since the end of the second world war.

The chart shows how commodities have shown strong growth on the back of the squeeze in prices caused by the supply chain issues. These issues emerged in 2021 which began the inflation tilt upwards. Then prices of commodities began to become exacerbated in 2022 due to the Ukraine conflict, which caused inflation to turn red hot.

Most of the global equity and bond markets are down this year. That’s because of uncertainties, primarily the effect of central banks raising interest rates, and their plans to raise rates further to tackle inflation. This, in turn, impacts the global economy and corporate earnings. In addition, the Russia-Ukraine war affects supply chains, the European economy and oil prices.

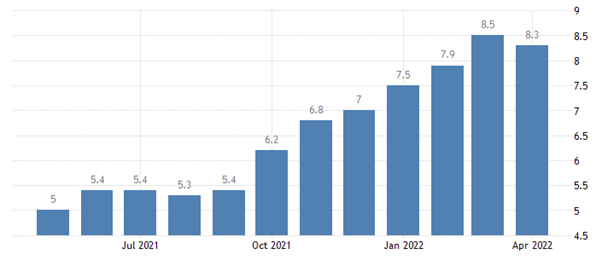

U.S Inflation

The chart below shows US inflation data. The annual inflation rate in the US slowed to 8.3% in April from a 41-year high of 8.5% in March. The index for gasoline (petrol) fell 6.1%, offsetting increases in the indices for natural gas (3.1%) and electricity (0.7%). The slowdown in April suggests that inflation has probably peaked. The speed at which inflation falls from here will be crucial, as it will lead to fewer interest rate rises, which will remove one of the market’s biggest concerns.

Despite all of this, there are many positives in the mix. I’ve listed examples below, ranging from a strong US labour market to an ever-growing market consensus about Fed rate policy.

1: US unemployment is low, companies are still hiring, and wage growth is solid:

- The current unemployment rate is 3.6%, very close to the pre-pandemic lows of 3.5%, and lower than at any point in the economic cycles of the 1980s (5.0% low), 1990s (3.8% low), or 2000s (4.4%).

- Last month, job openings hit a new record, at 11.5 million available positions. This would not happen if companies were worried about the economy or their future earnings power.

- Average hourly wage growth was 5.5% last month and had been tracking higher since the start of the year. This may not equal CPI inflation (8.6%), but it certainly helps offset it.

2: Markets may finally have a solid perspective on central banks’ intentions, removing a vital issue from investors’ “known unknowns” list:

- The US Central Bank Chairman Jerome Powell’s comments last week that the Fed is not considering 0.75% rate hikes at the next few meetings removed a significant point of uncertainty. As a result, markets now know there is a high probability that the subsequent two sessions will see 0.5% interest rate hikes. This will be priced into the forecasts and the models which determine the want and desire of investors to put capital back into the market or continue to remove their funds in a sell-off.

- Fed Funds Futures now shows 89% odds that Fed Funds will be 2.50-3.00% at year-end. This is the tightest range we’ve seen in weeks.

3: As stressed as equity markets may be about recession risk, corporate bonds are not:

- Investment-grade corporate bond spreads are 1.44 percentage points over Treasuries this week. Levels consistent with near or actual recessions start at 2.00 points and go up from there (2008, 2011, 2018, 2020).

- High-yield corporate bond spreads are 4.47 percentage points over Treasuries. Levels above 6.00 points signal recession or near-recession (same dates as IG spreads noted above).

4: Oil prices have stabilised:

- The highs for WTI crude ($124/barrel on the 8th of March) are now two months old.

- A strong dollar, a weak European economy and pandemic-related lockdowns in China are combining to keep global crude demand in check.

Overall

The point of this is not to call a bottom for US/global equities, but rather to remember that there are some positives out there. Many of the points above have one factor in common: inflation.

Takeaway: One data point does not make a trend, but it could be the start of a trend. Markets want to see inflation trending lower.”

If you would like to speak to one of our advisers regarding the current global markets, get contact us today.