How much should you have in your emergency fund?

The general rule of thumb for how much you should have in your emergency fund is 3 to 6 months of your current salary according to our in-house financial planners. With inflation hitting an all-time high and the risk of a recession on the horizon, it’s more important than ever to make sure you have funds in place if an emergency were to occur.

The pandemic was a recent example of a lot of uncertainty. For some, this time revealed hidden cracks and problems in their financial planning. Many were unprepared to face a complete global lockdown, which disturbed most sources of income. Against this background, the importance of planning an emergency fund has become clearer.

An emergency fund equips you with the stability to meet unexpected expenses and allows you to tide over hardships. Emergencies can take any shape, whether by way of

- Job loss

- Unexpected repairs

- Natural disasters

- An unexpected dip in business performance

- Unexpected travel

- Unplanned medical expenses

Therefore, such a fund is crucial to get started as soon as possible.

What makes an emergency fund, and why do you need it?

Your emergency fund should reflect your income and lifestyle.

- You should be able to rebuild it in case you need to use it

- It should also be easy to access

- It should not be used for anything other than an emergency

A sufficient fund that you cannot use when you need it serves no purpose. Once you create it, you might as well forget that you have it except for emergencies.

It is not quite possible to control every aspect of your life and future. However, you can take measures to ensure that you are safeguarded while facing adversities. The fund also protects your investment assets and savings. You don’t need to liquidate your assets for quick access to money. In the absence of an emergency fund, you may be forced to sell your investments when the market is already down. The impact is twofold:

- You lose out on the money that you could have made in better economic conditions.

- You’ll have to sell more assets to gather the emergency money you need.

How to create an Emergency Fund?

Build a budget

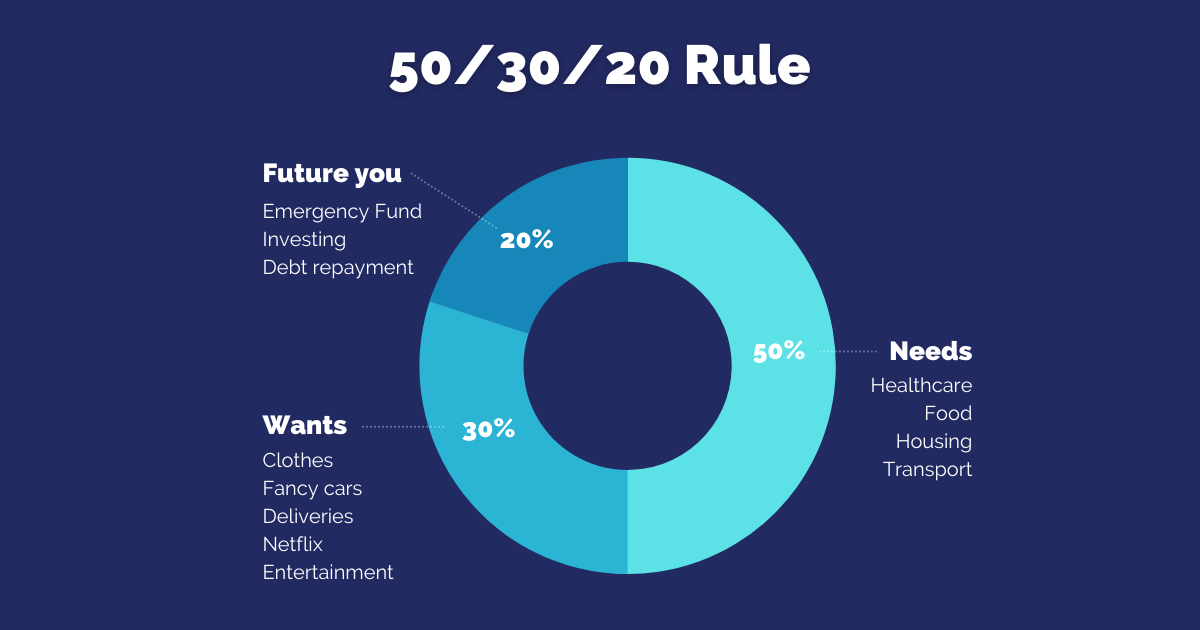

Look at your current finances, sources of income and expenditure, debt obligations, and assets. All of these will give you a brief snapshot of what your profile looks like. From this, calculate how much you can regularly contribute to the emergency fund. Use the 50/30/20 rule to break down your expenses and where you should be allocating money. See diagram below. This should help you plan how much money you will need to put towards your fund depending on your current living standards. Your circumstances are important to consider.

- Do you have any fixed source of income?

- Are you the sole earner of the family?

You may be tempted to plan big goals. However, it is the alternative route that you should adopt. Make a small but achievable goal. Not only will you be motivated to keep going when you achieve it but also build the discipline needed to work towards the bigger goal. As time goes by, set higher targets.

Keep an eye on the little details

It is easy to lose sight of details if you get lost in simply building the fund. It is also possible to lose progress. Therefore, there are a few things you should be careful about. Firstly,

- Automate your fund: Even if you forget those regular contributions, automation means that you won’t lose out on any benefits. You can have a standing instruction to have a certain amount deposited into the account.

- Don’t over save: You may reach your goals and keep going. An emergency fund is only for emergencies. You can use the remaining funds for other needs such as saving up for a house, building a retirement plan, and so on

- Check-in on your fund: Don’t forget about the fund. Like your investment portfolios, it’s important to review your needs and wants every 6 months.

Having 3-6 months of an emergency fund is a vital step in financial planning. If you would like to put a financial plan in place, speak to one of our advisers today. With tailor-made guidance on your finances, you can be better equipped to deal with current volatility.